Artificial Intelligence Technology Solutions — AITX — is one of those names where the hardest question is not whether the product works but whether the business model can ever carry the share count. The preliminary FY26 numbers disclosed this week show roughly 26% year-over-year revenue growth, which is a meaningful acceleration from the middle part of last year and is above the median growth rate of the broader security-robotics peer set. That is the good news, and it is genuinely good.

The less-discussed part of the same disclosure is the recurring-revenue (RMR) scale the company has now reached. AITX has crossed the threshold where the next set of investor questions stops being about whether ROSA and SCOT units are being deployed and starts being about gross margin per unit, support cost per deployment, and the absolute-dollar operating expense needed to sustain the growth rate. Those are different questions, and the answers to them are not yet in the public record.

The quick snapshot

Why RMR scale is the real milestone here

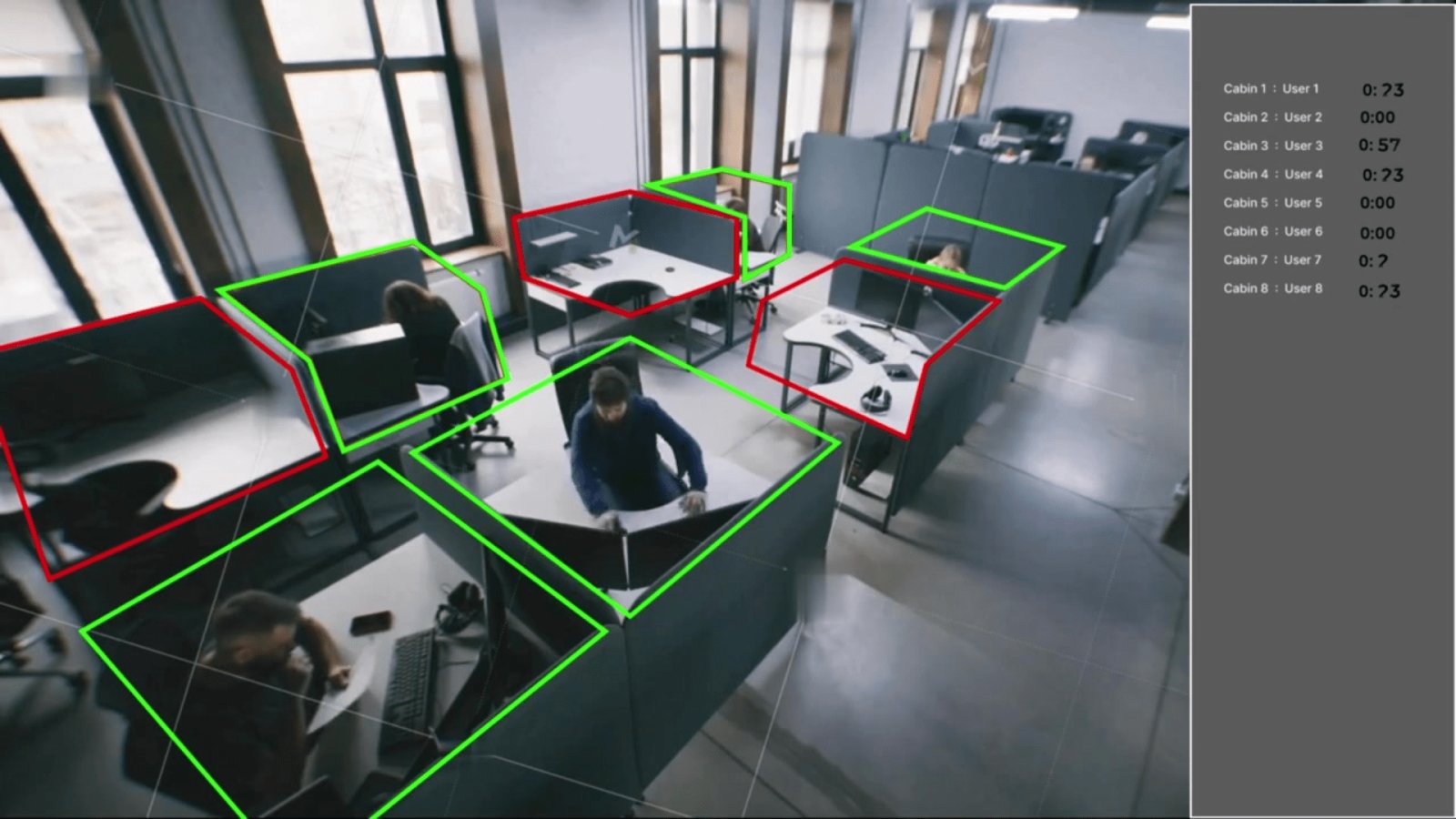

The recurring-revenue business model at AITX is the entire reason the stock exists. Hardware sales are capital-intensive one-time events; RMR contracts lock customers into monthly subscription fees for autonomous security platforms, and once those contracts are in place the revenue is highly sticky, the gross margin per unit should be high, and the lifetime value per customer looks attractive against customer acquisition cost.

The challenge, for several years, was that the RMR base was simply too small to matter against the operating expense base. That has now changed. With FY26 RMR now running at a scale that makes the unit-economics conversation real, the analytical question shifts from "is this a viable product" to "does the unit economics scale cleanly enough to produce absolute-dollar profitability." Those are different questions and require different disclosures to answer.

Growth trajectory versus cost base

The revenue-to-cost-base scissors are moving in the right direction. The share-count line is moving in the wrong direction. That is the whole tension of a neutral rating — the business is getting better, and the equity math is quietly getting worse at the same time.

What the market will watch in the full FY26 report

Preliminary disclosures are useful but incomplete. The full FY26 report, which will follow in the normal reporting window, is expected to surface three pieces of information that will either confirm or complicate the neutral read.

RMR gross margin is the single most important number in the filing, because it determines whether the recurring-revenue growth flows through to profitability at scale or whether a substantial portion is absorbed by field-service and support cost. Customer acquisition cost per deployment tells you whether the sales motion is efficient enough to sustain the growth rate without a proportional increase in the cost base. And the operating-cash-flow cadence — quarter by quarter — is the real-time signal of whether the business is approaching self-funding.

Why neutral, not bullish

Three reasons the rating is neutral rather than bullish, despite the legitimately above-sector growth.

- The scissors haven't closed. Revenue is still growing faster than OpEx, but not fast enough for the operating loss to narrow to the point of visibility on break-even. That gap matters in a name where the share count is continuing to expand.

- The "preliminary" qualifier. Preliminary numbers are directionally correct but typically lack the detail that would let a rigorous reader separate above-sector growth from subsidy-driven growth. That distinction is the one that matters for the equity multiple.

- Comparable-valuation drift. The security-robotics category has seen public and private comparables reset meaningfully over the last eighteen months. Even a well-executing company growing 26% does not automatically rerate in a category where the multiple has compressed.

The path to bullish

There is a clean path from "neutral" to "bullish" on AITX, and it does not require any heroic assumption. It requires two things: the full FY26 report to show RMR gross margin at a level consistent with eventual break-even, and a full quarter in which the share count line stops expanding. Both conditions are realistic within the next twelve months. Neither is guaranteed. The analytical discipline is to wait for the disclosure rather than anticipate it.

The bottom line

Preliminary FY26 is a legitimately good print in a sector where "good" has been hard to find. The question is no longer whether the company can grow; it is whether the growth translates into durable equity value at the current share count, and that question is not answerable until the full report arrives. Neutral is the honest rating, with a clear path to reconsideration.

Disclosure

This article is independent editorial content and reflects the author's opinion and analysis as of the date of publication. It is not investment advice and should not be relied on as the basis for any investment decision. MicroCap Desk and its contributors received no compensation of any kind — cash, securities, or otherwise — from any company mentioned, or from any third party, in connection with this article. The author holds no position in any security mentioned. Information is drawn from sources believed reliable but is not guaranteed accurate or complete. Microcap securities carry a high risk of loss. Do your own research. See our full Disclosure.